The defining feature of 21st-century geopolitical competition is the race to control dual-use infrastructure—systems that serve both civilian and military purposes. Whether in telecommunications, space-based assets, transportation corridors or energy networks, major powers are deploying civil-military infrastructure investments as instruments of long-term strategic influence.

This strategy is reshaping global power balances, rewriting supply-chain dependencies and redirecting capital flows toward firms positioned at the nexus of technology, security and national resilience.

1. Civil-Military Infrastructure as a Lever of Geopolitical Influence

Unlike conventional military assets, civil-military infrastructure is subtle, persistent and deeply embedded in the daily operation of global commerce.

Examples include:

5G and secure telecom ecosystems controlling data flows,

satellite constellations governing navigation, intelligence and logistics,

energy and smart-grid networks linking regions through dependency chains,

transport, port and undersea cable infrastructure shaping mobility and communication.

Control over these systems allows states to exercise influence without escalation—deterring rivals, shaping regulatory standards and constructing long-term technological dependence.

China’s Belt and Road infrastructure programs, the U.S.-Japan-Australia Blue Dot Network, and Europe’s Global Gateway all reflect this civil-military logic.

2. 5G Networks: Infrastructure as Strategic Architecture

5G systems, at their core, are command-and-control infrastructures underpinning both civilian industry and modern military operations.

Nations that secure dominance in 5G architecture can:

set cybersecurity norms,

constrain rivals’ access to telecom supply chains,

shape digital trade frameworks,

and preserve intelligence superiority through secured data channels.

This has spurred massive capital reallocation toward telecom-security firms and network integrators capable of providing trusted infrastructure, especially in Indo-Pacific democracies seeking alternatives to Chinese vendors.

3. Satellite Constellations: Space as the New Geoeconomic Platform

Low-Earth orbit constellations like Starlink, China’s GW system, and Europe’s IRIS² illustrate how satellite networks have become the backbone of both military operations and commercial connectivity.

Their dual-use functions include:

secure battlefield communications,

autonomous vehicle navigation,

maritime and logistics routing,

agricultural and climate monitoring.

The rapid scaling of satellite infrastructure has turned space-tech firms into high-value geopolitical assets, drawing investment from sovereign funds and defense-focused capital pools.

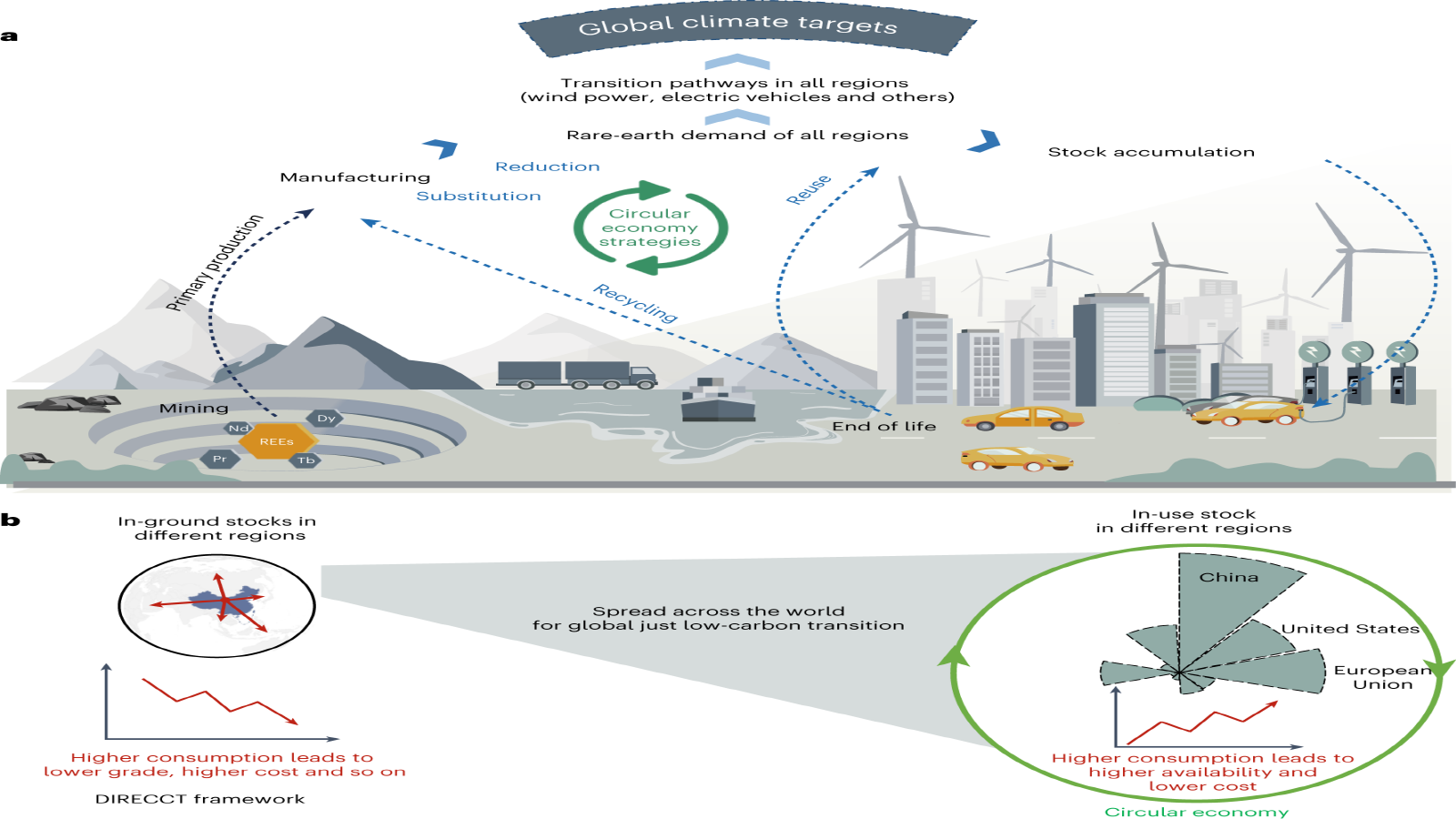

4. Energy Grids and Critical Mineral Supply Chains: Powering Influence

Energy infrastructure—especially LNG terminals, hydrogen networks, offshore wind grids and rare-earth supply chains—has become a battleground for strategic leverage.

Countries investing in cross-border energy grids gain:

political leverage over dependent states,

insulation from geopolitical shocks,

preferential investment inflows into strategic sectors.

Military-origin technologies, such as hardened grid-control systems and cyber-secured SCADA architectures, increasingly underpin these networks.

Their adoption enhances supply-chain resilience and attracts long-horizon institutional capital seeking safe harbors amid geopolitical volatility.

5. How Capital Markets React: Premiums for Strategic Infrastructure Firms

Global investors are placing premiums on companies integrating dual-use infrastructure capabilities.

Capital markets show three clear patterns:

(1) Reallocation toward resilient infrastructure assets

Firms providing secure telecom, energy and space-based infrastructure outperform broader market indices in periods of geopolitical tension.

(2) Surge of state-backed financing

Governments are co-investing in civil-military infrastructure firms, offering procurement guarantees and subsidy frameworks that de-risk private investment.

(3) Rising valuation of “strategic enablers”

Cybersecurity vendors, satellite operators, semiconductor foundries and grid modernizers receive capital inflows typically associated with high-growth tech sectors.

The message to investors is clear:

Strategic infrastructure is the new frontier of global competition—and a new source of return.

6. Supply-Chain Dependencies Rewired

Civil-military infrastructure alters supply-chain maps by creating:

trusted corridors (U.S.–Japan–Australia),

contested corridors (South China Sea, Arctic routes),

dependency corridors (energy networks, digital infrastructure).

These dependencies determine:

pricing power,

investment risk profiles,

corporate expansion strategies,

long-term geopolitical exposure.

Firms embedded within secure infrastructure ecosystems benefit from lower geopolitical risk premiums, while those reliant on rival-controlled systems face capital outflows.

Conclusion: A New Geoeconomic Doctrine

Civil-military infrastructure has emerged as a core strategic asset, redefining global power dynamics and financial-market behavior.

Nations that control dual-use networks—5G, satellites, energy grids, secure cables—gain disproportionate influence over the world’s economic arteries.

For investors, this marks the rise of geostrategic capital allocation: capital flowing not merely to efficient markets, but to secure markets.