For several years, strategic technology attracted capital through a familiar narrative: back the most promising platform early, scale quickly, and let commercial momentum do the rest. That logic is no longer enough. Across Europe and the NATO ecosystem, funding is being pushed into a more disciplined model, where public money, state-backed vehicles, and procurement-linked programs increasingly shape which technologies survive, scale, and matter.

This does not mean venture capital disappears. It means venture logic is being subordinated to strategic logic. NATO’s Innovation Fund is a €1 billion multi-sovereign fund designed to invest over a 15-year period in dual-use start-ups critical to Allied security, while DIANA now connects selected firms to accelerator sites, test centres, mentors, military end-users, and contractual funding. The signal to markets is clear: strategic technology is being financed less as pure speculation and more as a controlled pipeline from innovation to validation to adoption.

The European Union is moving in the same direction, but at much larger industrial scale. The European Defence Fund carries a budget of nearly €7.3 billion for 2021–2027, split between collaborative defence research and capability development, while the SAFE instrument is framed as the first pillar of Readiness 2030 and is intended to help unlock more than €800 billion in defence spending across the EU. EDIP adds another €1.5 billion layer focused on industrial modernisation, production ramp-up, resilience, and steady supply. That is not venture culture. That is state-backed capital discipline.

The policy tone matters as much as the headline numbers. In February 2026, the Commission amended the EDF Work Programme to simplify procedures for disruptive defence technologies and align the program with broader strategic technology investment tools. That suggests policymakers are no longer satisfied with merely funding innovation in principle. They are trying to reduce friction between public ambition and industrial execution. In practical terms, the question is shifting from “Which technology is exciting?” to “Which technology can move through a disciplined public financing and adoption process?”

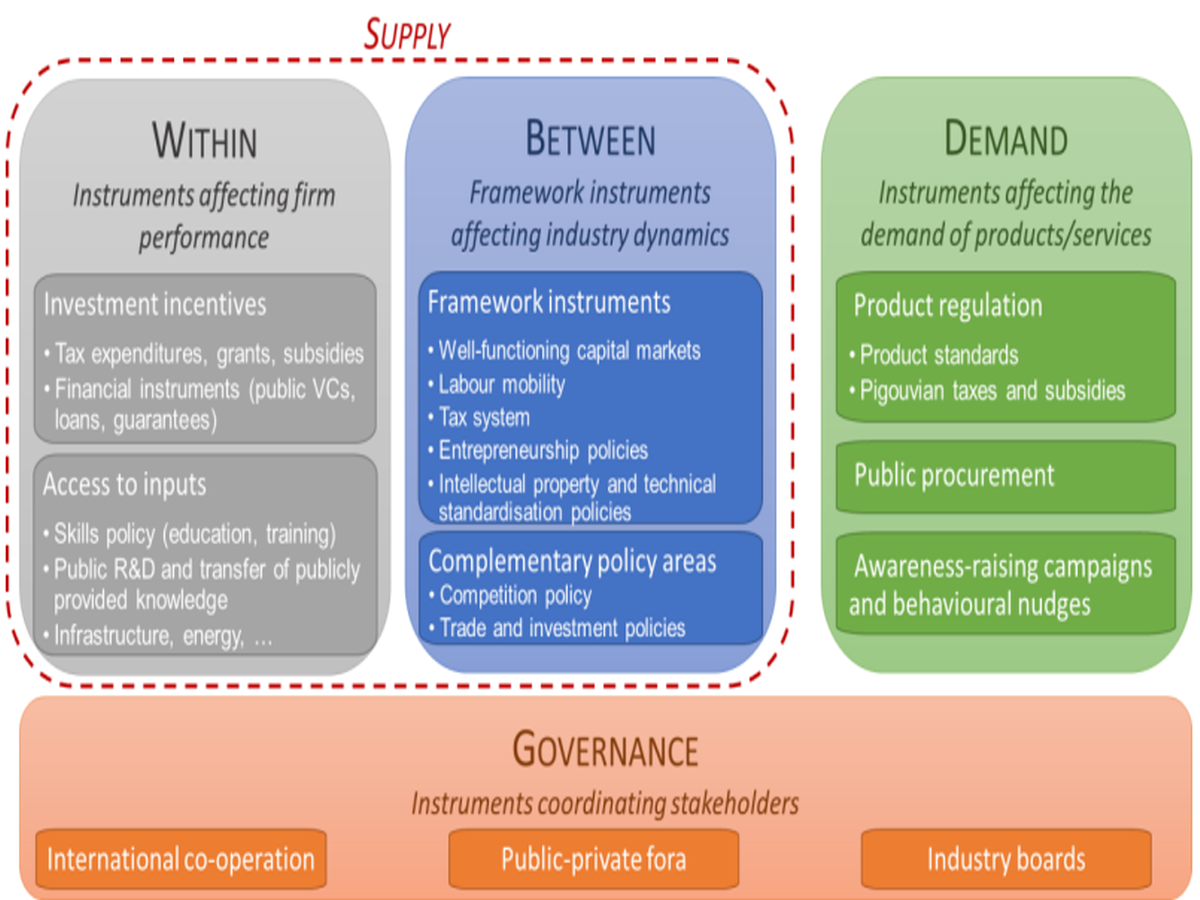

This broader shift also fits the OECD’s framing of industrial policy. OECD materials emphasize innovation and commercialisation, investment confidence, and strategic policy support as central levers for industrial development, while its industrial-policy work focuses on measuring how governments support business through targeted expenditures, delivery channels, and beneficiary design. That is important because strategic tech is increasingly being treated not as a free-floating market theme, but as an industrial-policy domain where state support, procurement design, and scaling incentives matter directly.

The market implication is straightforward. Capital is becoming less democratic and more directional. The winners may not be the firms with the loudest narratives or the biggest prototype hype. They may be the firms that can fit into public financing architecture, meet interoperability and compliance requirements, survive structured testing, and align with resilience goals in defense, energy, semiconductors, logistics, and dual-use manufacturing. That is partly an inference, but it follows directly from the way NATO, the EU, and OECD-linked policy frameworks are now organizing support.

For investors and operators, this changes the reading of “smart money.” In the previous cycle, smart money often meant private capital getting in before the crowd. In the next cycle, it may mean understanding where public money is building durable lanes for procurement, testing, production, and scale. State-backed discipline may sound less glamorous than venture hype, but it is more likely to determine which strategic technologies become institutions rather than headlines.

References

NATO, Defence Innovation Accelerator for the North Atlantic (DIANA).

NATO, Emerging and disruptive technologies.

NATO, NATO DIANA announces largest-ever cohort of 150 innovators for 2026.

European Commission, European Defence Fund (EDF) – Official webpage.

European Commission, SAFE | Security Action for Europe.

European Commission, EDIP | Forging Europe’s Defence.

European Commission, Changes to the EDF Work Programme for simpler procedures and expanded investment areas.

European Commission, Commission approves first wave of defence funding under SAFE.

European Commission, Commission approves second wave of SAFE defence funding.

OECD, Industrial policy.

OECD, Industrial policy for the future.

Socko/Ghost