In the Indo-Pacific theater, the long-running U.S.–China rivalry is no longer a diplomatic abstraction. It has become a powerful driver of corporate strategy and industrial supply chain restructuring, particularly for firms with exposure to semiconductors, electronics manufacturing, and defense technologies.

The regional diversification of supply chains reflects more than geopolitical signaling. Companies with strategic technologies are being compelled to rebalance production footprints, secure alternative sourcing, and reduce dependencies on China-centered networks—a shift that is now influencing capital flows and competitive positioning across global markets. trendsresearch.org+1

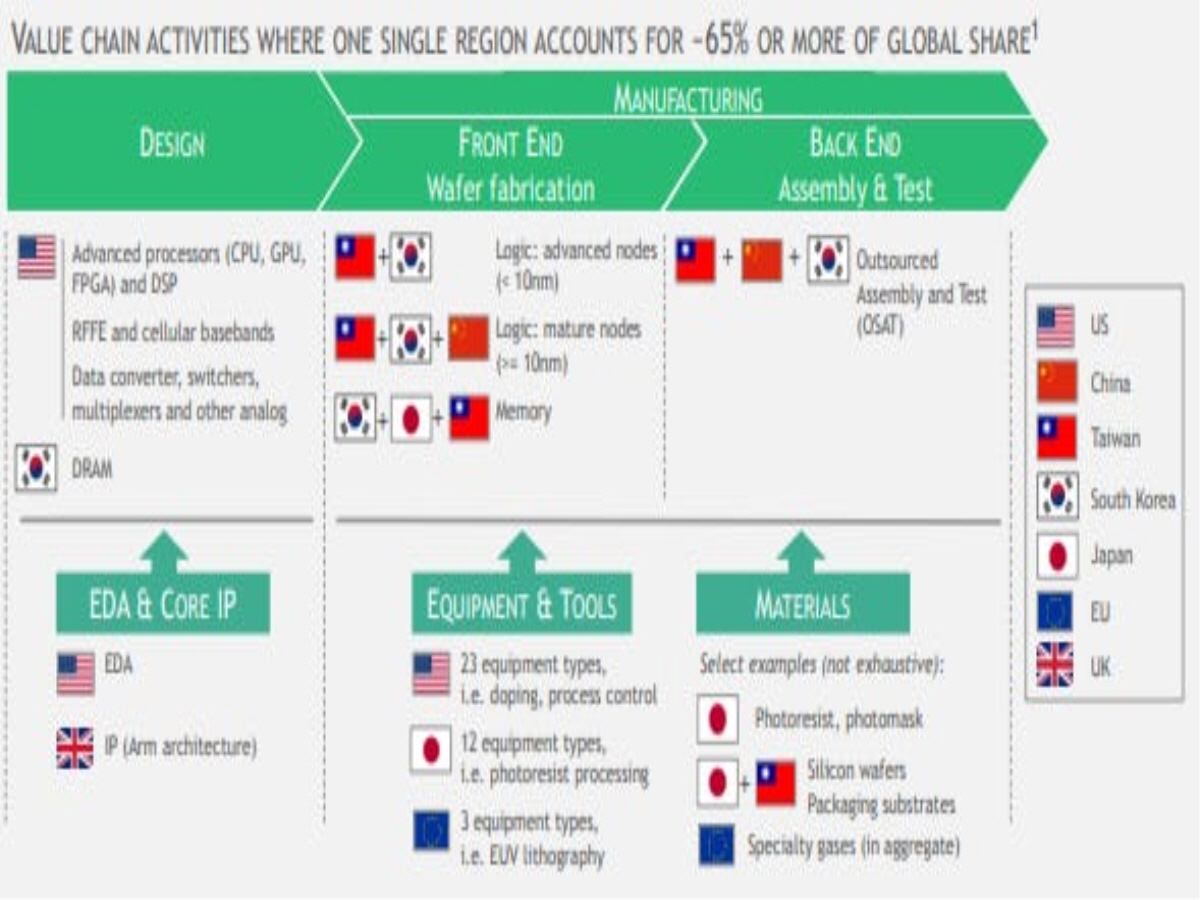

TSMC (Taiwan Semiconductor Manufacturing Company): From Risk Zone to Strategic Hub

The world’s most advanced logic chips are overwhelmingly produced by Taiwan Semiconductor Manufacturing Company. A recent disruption—such as the April 2024 earthquake that briefly shuttered TSMC facilities—highlighted how concentrated semiconductor output can imperil global technology supply chains. saisreview.sais.jhu.edu

To mitigate such systemic risk, TSMC is expanding fabrication capacity in Japan and the United States, and accelerating investments in India. These moves reflect a broader industry trend in which major chipmakers pursue a “China+1” diversification strategy—maintaining existing bases while building alternative capacity outside China. trendsresearch.org

The strategic implication is clear:

TSMC’s production realignment enhances its resilience but also strengthens the technological autonomy of U.S. allies and partners in the Indo-Pacific. That, in turn, embeds TSMC deeper into defense and critical infrastructure supply networks—far beyond its commercial consumer electronics market.

Foxconn: Diversifying Electronics Manufacturing Beyond China

Another pivotal player is Foxconn, known for assembling iPhones and other consumer devices. Foxconn has significantly shifted capacity toward India and Southeast Asia, driven by rising labor costs in China, U.S.–China trade tensions, and customer demand for supply-chain resiliency.

This “China-plus-regionalization” strategy not only hedges geopolitical risk but also positions Foxconn as a key partner to global OEMs seeking industrial footprints aligned with Western and Indo-Pacific trade frameworks. trendsresearch.org

For Foxconn, such diversification is not purely defensive. It offers competitive leverage with major Western customers and opens access to new markets in India, ASEAN, and beyond—turning supply-chain reform into revenue growth.

ST Engineering: Building Defense and Tech Production in Emerging Indo-Pacific Centers

In defense and integrated systems, Singapore’s ST Engineering exemplifies a strategic response to the evolving supply landscape. Leveraging its diversified portfolio across digital, land, air, and sea domains, ST Engineering has expanded in-country production arrangements with partners such as Kazakhstan and other Indo-Pacific states. wikipedia

This approach reflects a broader shift away from centralized manufacturing toward regionally distributed value chains that align with political risk profiles and alliance structures. For ST Engineering, this means securing production capacity in multiple jurisdictions, reducing vulnerability to regional disruptions, and embedding itself more deeply in allied defense ecosystems.

Rare Earths and Critical Inputs: The Case of Vulcan Elements

Beyond final assembly, critical inputs such as rare earth magnets are increasingly in focus. Vulcan Elements, a U.S. rare earth magnet producer, recently secured a major Department of Defense-backed loan to expand domestic output—explicitly aimed at reducing dependence on foreign mineral supply chains that China dominates. wikipedia

This illustrates how supply-chain diversification now reaches raw materials and strategic components, not just finished goods. Companies that can localize or regionalize such critical nodes gain both market and geopolitical leverage.

The Broader Strategic Realignment

The corporate strategies of TSMC, Foxconn, ST Engineering, and Vulcan Elements underscore a larger pattern:

- Partial decoupling of China-centric supply chains in critical technologies is underway. Asian Journal of Peacebuilding Vol. 10 No. 2 (2022)

- Alternative production hubs—India, Southeast Asia, Japan, and U.S./Europe partnerships—are rapidly gaining traction. trendsresearch.org

- Indo-Pacific nations pursue multi-alignment strategies, balancing ties with the U.S., China, and other partners to extract economic benefits while managing risk. Pacific Forum

This realignment is not merely defensive. It is reshaping capital allocation, industrial specialization, and strategic influence in global technology sectors.

Strategic Implications

For investors and corporate planners, the implications are profound:

- Future value will be concentrated among firms that operationalize diversification early.

Firms that embed supply-chain resilience into their core business models capture both market share and strategic partnerships. - Geopolitical alignment shapes technology ecosystems.

Companies must choose where to build capacity based on alliance frameworks and regulatory environments—not just pure cost metrics. - Critical technology networks will bifurcate.

One set oriented toward U.S. and allied markets, another toward China and its partners.

In the Indo-Pacific economic order, supply-chain strategy is a strategic asset—no less than intellectual property or brand equity.

Socko/Ghost